How to Pass Accounting Entries Under GST?

The goods and services tax, also known as the GST, was implemented to replace the majority of indirect taxes in India. In India, we currently have a system known as "One Nation, One Tax"

However ,the regular GST accounting entries in accounts, including purchase entry with GST and GST purchase entry, must be understood and passed through to the accounting department. If you are filing GST returns, such as GSTR-1, and GSTR-2B, it is critical to ensure no conflicts as possible between your books of accounts and your GST reports. The proper and timely reconciliation of accounts in necessary for preparation and filing of GSTR9

GST Accounting

During Pre-GST Era, Excise, VAT, CST, and Service tax all taxes used to mandate preparation of their own set of accounts and in addition to that, you could not claim the input tax credit for both central and state-imposed taxes. As a result, multiple ledger accounts were required to be created and maintained in the books of accounts. However, accounting for GST journal entries, including purchase entry with GST example, has eliminated the necessity for several ledger accounts ,reducing the number to just a handful of accounts.

In addition to the accounts like stocks, sales, and purchase journal entries with GST had to keep only a few ledger accounts under the former regime:

- Excise payable a/c (for manufacturers)

- CENVAT credit a/c (for manufacturers)

- Output VAT a/c

- Input VAT a/c

- Input Service tax a/c

- Output Service tax a/c

For example, a trader named Mr. Suresh is required to keep the following basic ledger accounts:

- Output VAT a/c

- Input VAT a/c

- CST A/c (for inter-state sales and purchases)

- Account for Service tax

Looking for expert support with accounting services? Click here to learn how we can help streamline your financial processes.

Accounting Under the GST Regime

Previously separate indirect taxes like VAT, and Service Tax are now combined under GST. For each GST Number (GSTIN), the same trader, Mr Suresh must keep the following accounts:

- Input CGST Account

- Output CGST Account

- Input SGST Account

- Output SGST Account

- Input IGST Account

- Output IGST Account

- Input Cess Account

- Output Cess Account

- Electronic Cash Ledger (to be kept up to date on the government's GST portal in order to deposit and pay GST in cash)

After accounting for GST journal entries and understanding their work, it will be much easier for you to maintain track of your data. When Mr Suresh can deduct his input tax on services from his output tax on sales of products, he will reap significant financial benefits.

Every business owner must keep track of the following accounts:

- A stock account that keeps track of the things that have been bought and sold. Among the information in this account should be the opening balance, the number of products received and delivered, the balance stock of raw materials and finished goods, scrap and wastage, and any other information relevant to the business.

- Records of any loans made and received, as well as records of any payments made and received.

- The tax account contains data on taxes owed, taxes collected, input tax, and tax credits claimed. Details about the provider, such as the supplier's name and address, are required from whom the taxable goods or services were purchased.

- Identifying information about the recipient, such as the buyer's name and address and the products or services delivered.

It is necessary to provide a warehouse or garage or any other location where the items will be kept. Commodities in transit and information about the stock that was accessible at the time are included in this category.

Monthly accounts contain the quantitative information as follows:

- Creating raw materials for the manufacturing industry

- Manufactured products are items that have been created by hand.

The accounts must include quantitative information on things that were utilized in the provision of services and information on input services that were used and services supplied.

Also Read: Input Service Distributor

How to Pass Accounting Entries Under GST?

Each type of GST: CGST, SGST, and IGST are processed differently when calculated in the books. Let's take a look at some sample data to understand how the input GST and the output GST are passed.

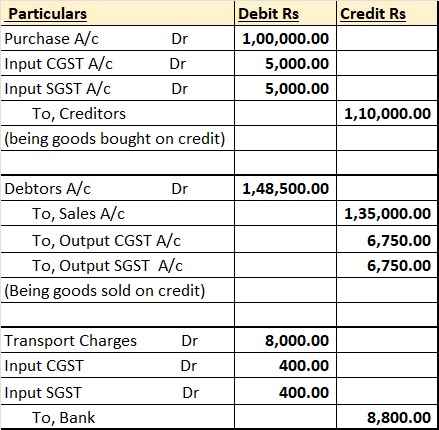

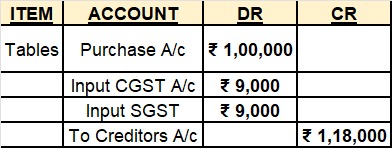

Let's say Ram spends ₹ 1,00,000 on a tables from a GST registered supplier in the state. The tax on his purchase is 18% and is divided into CGST (9%) and SGST (9%). Asa result, he pays a total tax of ₹ 18,000 (18% of ₹ 1,00,000) evenly divided between CGST (₹ 9,000) and SGST (₹ 9,000). If he needs to offset the sales tax, he can claim this amount as a sales tax credit.

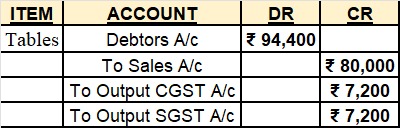

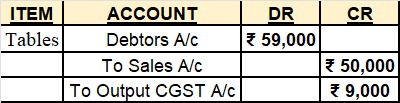

If an individual sells these tables to another GST registered seller, the transaction is recorded on sales A/ c and the submitted CGST and SGST are used for accrued sales tax. In this case, the creditor will eventually become the debtor.

For clarity, CGST and SGST are levied as temporary sales tax on the purchase of goods and services, while output tax is levied on the sale of goods and services. Therefore, deduct outgoing and incoming GST, net CGST, and net SGST.

Net CGST payable = Output CGST – Input CGST

Net SGST payable = Output SGST – Input SGST

Suppose Ram spends ₹1,00,000 on a table from a GST registered vendor outside its jurisdiction. A tax rate of 18% is levied on his transactions. As a result, he pays ₹ 18,000 (18% of ₹ 1,00,000) at IGST and can use it as his entry balance.

His tables are sold for ₹ 50,000 outside of his state. An IGST of 18% of ₹ 50,000, or ₹ 9000, will be the output tax due for these.

Each registered taxpayer must maintain an account for five years from the due date of the annual tax return for the year. At the end of the fiscal year, taxpayers must check the ledger against the GST tax returns filed throughout the fiscal year. When comparing the data between the books and the inputs and outputs of the GST tax return, the book discrepancies must be corrected or disclosed in subsequent GST forms.

Accounting for Purchase Entry With GST

To accurately record a purchase entry in Tally with GST, two accounts must be debited. First, debit the expense or asset account for the net cost of the purchase. Next, debit the GST input tax account for the GST amount paid. On the credit side, if the payment is made immediately, credit the cash account; if the purchase is on credit, credit the accounts payable account instead. This double-entry system ensures that total debits match total credits. When entering transactions in Tally ,ensure that GST configurations are properly set up for accurate reporting and compliance.

● Ensure the GST charge is accurately deducted from the net purchase amount.

● Verify that the applied GST rates comply with current tax regulations.

● Enter the GST amount in a separate input tax account for easy credit claims.

● Maintain detailed purchase records to support entries during audits or inspections.

Key Steps to Record a Purchase Entry with GST in Accounting Journal

Step1: Debit the relevant expense or asset account. This represents the total amount excluding GST.

Step 2: Debit the GST input tax account to record the GST component separately.

Step 3: Credit the cash or accounts payable account. This includes the total cost along with GST.

Illustration: Suppose a company purchases office equipment worth Rs.2,000, with a 12% GST of Rs. 240.

● Regarding Office Equipment (Expense or Asset): Debit Rs. 2,000

● Regarding GST Input Tax: Debit Rs. 240

● Regarding Cash or Accounts Payable: Credit Rs. 2,240

This entry helps in accurate bookkeeping and GST compliance. If you're wondering how to record purchase entry in Tally, ensure GST settings are enabled and select the appropriate tax ledger while making the entry.

Before GST: Accounting Under Excise and VAT

Before GST was implemented, taxpayers had to manage multiple accounting systems for different taxes like Excise, VAT, CST, and Service Tax. Maintaining separate accounts was essential, and claiming an input tax credit across central and state taxes was not possible. This complexity required businesses to maintain several ledger accounts.

With GST, the need for multiple ledgers has been significantly reduced, simplifying accounting processes. Below are some of the key ledger accounts that businesses had to maintain under the previous tax system, apart from purchase, sales, and stock accounts:

● Excise Payable A/C (Manufacturers)

● CENVAT Credit A/C (Manufacturers)

● Input VAT A/C

● Output VAT A/C

● Input Service Tax A/C

Impact of GST on Profit & Loss Account and Balance Sheet

GST has minimal impact on the Profit & Loss (P&L) account since tax accounts do not directly relate to business income or expenses. However, any GST paid without an input tax credit claimable must be recorded as an expense, reducing profits. The Balance Sheet, on the other hand, should reflect the tax liability or the eligible input tax credit as either a liability or an asset. Fixed assets eligible for an input tax credit should be recorded at cost, excluding GST.

GST Returns and Corresponding Entries

Businesses must file different types of GST returns, each serving a unique purpose in tax compliance and reporting:

● GSTR-1: Captures details of all outward supplies (sales) made during the month. It plays a crucial role in determining the tax liability of a business.

● GSTR-3B: Summarizes the total taxable turnover, claimed Input Tax Credit (ITC), and tax liability. This return is filed either monthly or quarterly and is essential for tax payments and compliance tracking.

● GSTR-9: Acts as an annual reconciliation statement that consolidates data from GSTR-1 and GSTR-3B, ensuring all tax, ITC, and liability details align accurately.

Retention of GST Records

Every registered taxpayer must maintain GST-related records for at least five years from the due date of filing the annual return for that financial year. At the fiscal year-end, businesses must reconcile their books with GST returns. Any discrepancies found must either be corrected in the books or appropriately disclosed in future GST filings.

Conclusion

The goods and services tax (GST) was implemented in India on July 1st. As a result, the GST Council has been trying to simplify the rules to make doing business easier, and streamlined GST inputs help us understand transactions more straightforwardly. In India, the Customs and Excise Act is a comprehensive, multi-category tax on all value additions tax-deductible to the extent allowed by law. The GST journal entry and the purchase entry with GST or the sales entry with GST are the same.

FAQs

Q: How does the GST liability ledger function and what is it?

Ans:

The computerized liability ledger displays the total amount of tax owed by the registered taxpayer as well as the input and output GST entries. The information in this ledger relates to the GST liability. It demonstrates explicitly how the GST liability was reduced by using cash or credit transactions.

Q: How do you account for the goods and services tax (GST)?

Ans:

Every registered taxable person is required to maintain their records of GST accounting entries for at least six years after the date the applicable annual return was filed under the goods and services tax (GST) law. These documents and supporting materials must be kept on hand at each of the business locations specified on the registration certificate, including the main site.

Q: How should a GST journal entry be passed?

Ans:

The output balances are transferred to the amount of utilization, per the calculations. Debit, the user account's final balance, is moved to the GST input account. For GST payments, the remaining balance in the output accounts will be transferred to the GST payable account.

Q: What is the accounting entry for the goods and services tax?

Ans:

Under the GST regime, several traditionally distinct indirect taxes, such as excise, VAT, and service tax, have been consolidated into a single account