In this article we shall go into detail about to understand the meaning of an input service distributor or ISD. Input Service Distributor is anindividual in charge of distributing the GST input tax credits. It is an responsibility of input service distributor or ISD to maintain tax credits to any company's GSTIN or to any company's branches with a different GSTIN but registered under the same PAN number

Do you know?

Registration with the ISD is required under Section 24 of the GST Act. You must submit your registration request using the form GSTREG-01.

Who Is an Input Service Distributor in GST?

An individual taxpayer known as an input service distributor is in responsibility of being the first to receive all of the bills for the services used by a company's branches. The ISD's responsibility is to disburse the Input Tax Credit, a tax that must be paid (ITC). However, it is required that the branches have the same PAN as the ISD. The company that needs its services to be paid should have different GSTINs.

An ISD under the GST is defined as follows in Section 2(61)of the CGST Act, 2017:

- It is a representative with authority from a supplier of products and services.

- In exchange for his services, this official receives tax invoices.

- He is in charge of allocating GST/CGST/UTGST credit to a supplier of products who has the same PAN.

- Additionally, he sends out bills to distribute credit.

Under GST, an ISD may operate from multiple locations, including a head office, registered office, branch office, etc. He can pay the tax for all of these services as well as a variety of input services, courier costs, housekeeping costs, and security fees. Such a person is eligible to apply for the GST status of Input Service Distributor.

To know more about GST read : Basic Of GST

Situations where ISD under GST Is not applicable?

The ISD under GST is not permitted to disburse the input tax credit in a few specific circumstances:

- It is a representative with authority from a supplier of products and services.

- In exchange for his services, this official receives tax invoices.

- He is in charge of allocating GST/CGST/UTGST credit to a supplier of products who has the same PAN.

- Additionally, he sends out bills to distribute credit.

The Purpose of Registering as an ISD under GST

Companies with numerous locations or worldwide operations frequently concentrate on sourcing their products or services from a particular sector. In such circumstances, the GST input tax credit acquired by the purchasing agency must be given to the branch in accordance with the use of services in order to effectively erase the GST tax.

In this case, the taxpayer may sign up as an Input Service Distributor with the centralized purchasing office. By sending an invoice to the branches once the purchases are done, the ISD under GST can transmit the IGST, CGST, and SGST tax credits. One essential component of ISD registration under GST is that it only applies to the tax on input services. Only the tax under input services, according to ISD, can be distributed. The input tax credit for input products and fixed assets cannot be distributed by the input service distributor.

The ISD mechanism in the GST is a clause created for companies that have a variety of shared expenses. These businesses use a centralized system for processing payments and bills from one place. The distribution of input services is designed to make the credit-taking procedure easier. According to the GST regulations, the entire idea is supposed to improve the easy flow of credit.

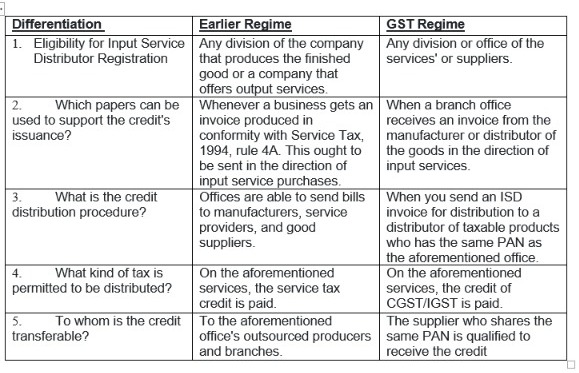

Insight on Input Service Distribution in GST under Earlier Regime and GST Regime

These are the main and most crucial areas of distinction between the two regimes. The distribution of credit is restricted to offices or branches with the same PAN, as was previously stated. This idea's justification is the transfer of taxation credit from manufacture to supply. The increase in tax liability at the time of supply was a result of the previous regime. In the end, ISD would pay taxes under the GST utilizing the applicable input tax credit.

Invoicing

Only by issuing the tax credits as an ISD invoice can the distribution of credits be carried out.

Returns

To guarantee that the tax credit available to the input service distributor at the end of the month is not exceeded, the ISD under GST must monitor the credit amount. The GSTR-6 form for this distribution of credit funds must be submitted by the 13th day of the subsequent month.

The GSTR-6A, which is auto-populated from the supplier's return, contains information about the tax credit that ISD has distributed to the tax credit recipient. It can then be claimed by the recipient branch by including a statement in GSTR-3B. Every year, an ISD is not obliged to submit Form GSTR-9.

Distribution of ITC

The tax credit is ineligible for transfer to the receivers via the reverse charge method. In this instance, the input service distribut or must apply for this credit just like any other taxpayer.

FAQ's

Q: Do ISDs need to be registered individually with GST?

Answer: Yes. Registering a specific ISD for a taxpayer facility is an additional step in registering as a regular taxpayer.

Q: Is it mandatory to distribute credits only to units that generate revenue through ISD under GST?

Answer: Only GST obligations are revenue-generating units. Therefore, according to regulations, ITCs on the services consumed by these entities should be used to offset them when they declare their tax obligations.

Q: Can taxpayers have multiple ISDs under GST?

Answer: Yes. Various taxpayer offices are eligible to apply for ISD registration under the GST.

Q: Is ISD registration required for GST?

Answer: Input Service Distributor must be registered as an ISD under the GST. This registration is an additional process after entering the service distributor as a regular taxpayer in the GST registration. This type of taxpayer must register as an ISD with GST using serial number 14 on the REG-01 form. Only after the registration process above, is the Input Service Distributor is authorized to distribute credits to recipients.

Q: What is a GST Input Service Distributor?

Answer: The Input Distributor is the authoritative officer responsible for distributing the GST Input Tax Credit. A GST-based ISD is responsible for maintaining a GSTIN tax credit for each company or branch office of a company that has a different GSTIN but is registered with the same PAN number.

Conclusion

The procedure for decreasing the credit will not change in the case of ITCs distributed by input service distributors under GST. For companies that prioritize centralized payments from any of their branch offices, the idea of ISD under GST was established to make credit distribution simpler. The distribution of the Input Tax Credit falls within the purview of the Input Service Distributor, who is accountable for issuing an agreement detailing the precise ITC distributed.

Experiencing difficulties? Jordensky is here to assist you, a friend in need and one-stop shop for all problems relating to Accounting, income tax or GST filing, and more. Try it now!

About Jordensky

At Jordensky, we are committed to providing an experience of the highest caliber while specializing in accounting, taxes, MIS, and CFO services for startups and expanding businesses.

When you work with Jordensky, you get a team of finance experts who take the finance work off your plate– ”so you can focus on your business.”