Liked our Blogs?

Please share your details to Subscribe to our Newsletter

Oops! Something went wrong while submitting the form.

In India, payroll accounting is governed by a complex set of laws and regulations, and it is crucial to ensure compliance

As an expert in payroll accounting in India, I am excited to share my knowledge and insights on this important topic. Payroll accounting involves managing and tracking the financial aspects of an organization's employees, including their salaries, bonuses, and deductions. In India, payroll accounting is governed by a complex set of laws and regulations, and it is crucial for businesses to ensure compliance in order to avoid penalties and legal issues.

This article covers all that you want to realize about finance bookkeeping. Here, we'll discuss the extent of work, sorts of sections, and the distinction between finance liabilities and costs. You'll likewise figure out how to set the progression of your finance cycle to oversee difficulties experienced with finance bookkeeping.

So, let's get started!

Finance accounting involves following, recording, and paying employees for a given time frame. In view of the definition, the finance cycle incorporates the accompanying essential undertakings:

But payroll doesn't stop there. It also includes performing the following accounting functions:

Payroll has a wide range of tasks. This includes high-volume financial transactions that require recording, archiving, and payment in order to make payments. Below is a list of financial items that should be included in your payroll.

Auditors and accountants must accurately manage all payroll-related financial transactions, whether assets or liabilities. Accounting software and other payroll automation tools can be used to help with this.

Accurate financial records are key to a streamlined payroll process. Before paying employees and paying taxes, accountants must ensure that all financial transactions are recorded.

Here are the types of payroll entries your business should consider:

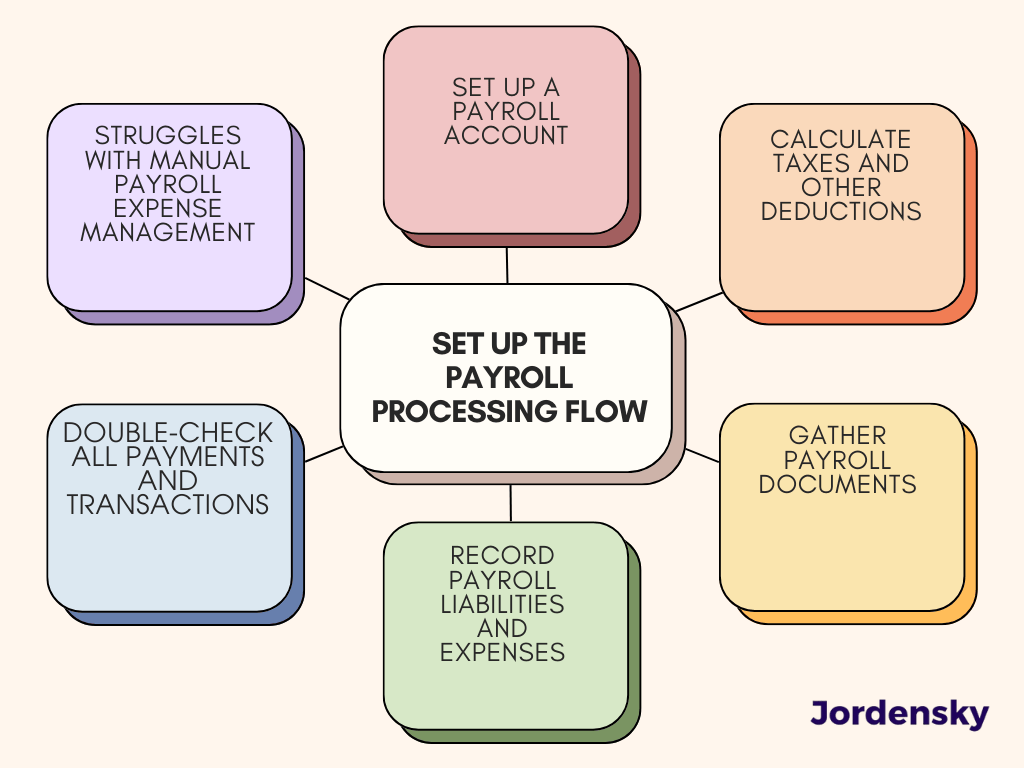

Now that we've covered payroll concepts, it's time to establish a payroll process flow. Complete the following steps.

Start setting up your payroll account for your business. Todo this, you first need to decide how you will reward your employees. Employee wages, payment deadlines, benefits and tax obligations must be considered.

We recommend using automated tools or software for proper bookkeeping. Investing in the latest technology allows accountants to streamline the payroll process and keep everything perfectly organized.

As soon as you have a payroll account, the calculation starts. First, prioritize employee taxes and other important deductions. Then enter the data into the billing tool for automatic calculation and payment.

Understand that we withhold taxes from our employees salaries to cover our Income Tax, Social Security and Medicare tax liabilities. Also include deductions from employee payroll as payments for employee benefits, retirement plans, health insurance, dental insurance, vision insurance, and life insurance.

At this point, the accountant can go ahead and collect all payroll records. Be sure to collect all forms submitted and submitted by your employees. They must be scanned and entered into the payroll system for record keeping.

Payroll documents include Form I-9 (Verification of Employment Eligibility), Form W-4 (Employee Tax Status), and Direct Deposit Authorization Form (for checks deposited into employee accounts).

If payroll accounts are set up, accountants must track all payroll obligations and expenses. Set up a Chart of Accounts (COA) to record and monitor all financial transactions.

We recommend using accounting software for automatic payroll. You can also make informed business decisions with accurate financial reporting.

With ongoing financial transactions and regular payroll payments, it is important to verify your payroll account. Indeed, automated accounting software can make accurate calculations. However, it still requires human intervention and regular audits.

While accountants record financial transactions (including payroll obligations), accountants review, analyze, and report on the financial condition of the business. So consider hiring these professionals for your business.

As previously mentioned, 25% of small businesses still do manual bookkeeping and bookkeeping. This has some potential drawbacks that can put your business' finances at risk.

Manually processing payroll is cumbersome and cumbersome. Here are some issues that can arise with manual management:

Automating payroll and other accounting functions can provide several benefits to an organization. Here are a few examples:

Overall, automating payroll and other accounting functions can help organizations operate more efficiently, accurately, and securely.

Here are some frequently asked questions (FAQs) about payroll accounting:

Q: What is payroll accounting?

Payroll accounting is the process of managing and tracking the financial aspects of an organization's employees, including their salaries, bonuses, and deductions. This involves calculating pay, withholding taxes and other deductions, and providing employees with pay stubs or other documents detailing their earnings and deductions.

Q: What is included in payroll accounting?

Payroll accounting typically includes calculating an employee's gross pay, subtracting taxes and other deductions, and issuing net pay. It may also involve tracking and reporting on employees' paid time off, such as vacation and sick leave, as well as calculating and paying bonuses and other forms of compensation.

Q: Who is responsible for payroll accounting?

The specific person or team responsible for payroll accounting will vary depending on the size and structure of the organization. In a small business, the owner or manager may be responsible for payroll accounting, while in a larger organization, there may be a dedicated payroll department or team.

Q: What are the benefits of payroll accounting?

Payroll accounting offers several benefits, including ensuring that employees are paid accurately and on time, tracking and reporting on employee compensation and benefits, and providing a clear record of earnings and deductions for tax and other purposes. It can also help organizations avoid penalties and legal issues related to payroll.

Q: What are some challenges of payroll accounting?

Some of the challenges of payroll accounting include staying up-to-date with changing laws and regulations, ensuring compliance with tax and other requirements, and managing the complexity of payroll for organizations with multiple locations or employees with different pay rates and benefits. Additionally, payroll errors can be costly and time-consuming to correct.

Payroll is an integral part of a company's success. It's not just about paying employees correctly and on time. Tracking salaries, benefits and taxes. It is also important to manage cash flow and maintain financial health.

For payroll, follow the recommended steps to set up your payroll process and solve some common challenges. Also, be sure to automate your payroll system and invest in accounting and other financial software.

Optimize your payroll by making well-founded decisions. Accurate, efficient and seamless payroll guarantees employee satisfaction and business success!

Also Read,

8 Most Common Accounting Mistakes and how to avoid Accounting Errors