Common Accounting Mistakes and How to Avoid Them

Accounting system is the key to understanding the financials status of any company. Maintaining accounts is also necessary for tax preparation and other government compliance compliances. Unfortunately, accounting errors can occur whether accounting software is a cloud-based or desktop accounting solution.

It is crucial to understand what can go wrong with accounting and how it can affect your business and even more crucial is understanding how to find and rectify accounting errors and avoid future one

Understanding the Significance of Accurate Accounting

From early manual record keeping, accounting has grown into a vital tool for tracking financial health and business performance. Accuracy in accounting is more important than ever in the fast-paced economic environment since it has a direct impact on a company's financial health, operational efficiency, tax obligations and regulatory compliance. However, accounting mistakes can occur in both cloud and desktop systems. Maintaining transparency and long-term success requires an understanding of accounting errors, their effects, and the application of efficient error detection, error correction and preventive measures.

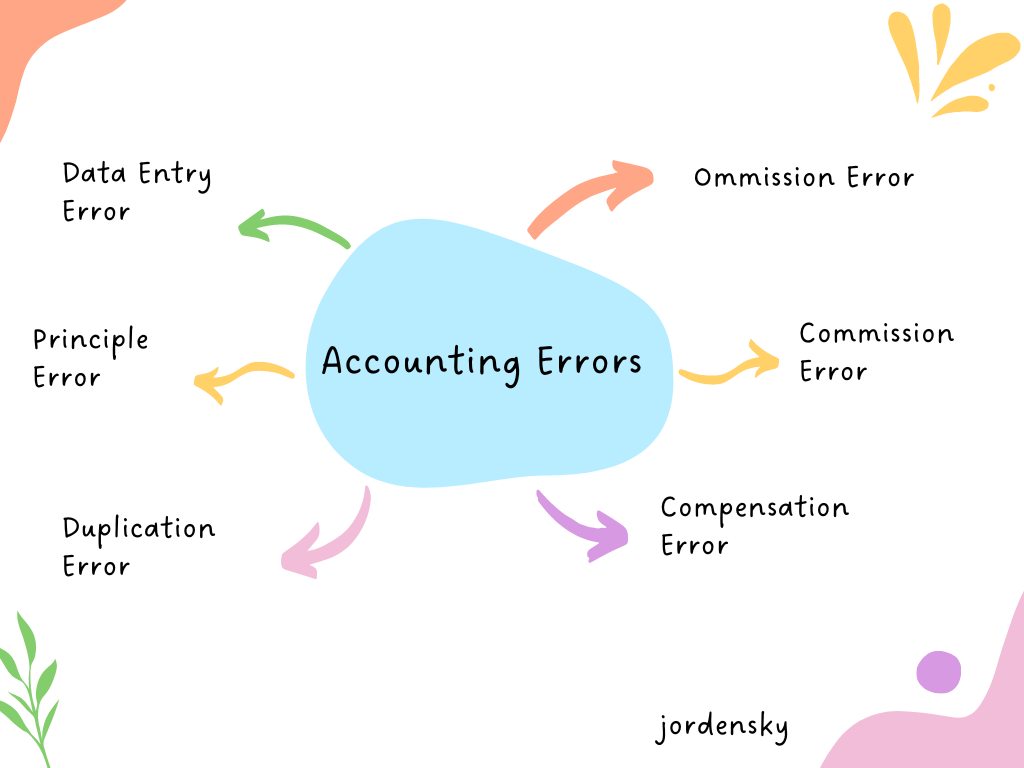

Most common type of Accounting Errors

The integrity of your accounting system's information is only as good as the data you submit. This includes adding an item to the proper account, assigning the item the correct description or code, and entering the correct amount.

Accounting errors, unfortunately, can arise from simple blunders or misunderstandings of accounting principles. When analyzing accounting reports, watch for the following sorts of errors.

1. Data Entry Errors

Data entry errors occur when and where items are entered (or not recorded) in your accounting system. The following are some examples of common data entry errors:

- Items are being entered into the incorrect account.

- Number transposition

- Removing or adding a number or decimal place

- Leaving out or duplicating an entry.

- Considering expenses to be income or vice versa.

2. Omission Error

This is merely an error in recording an item. It's not on purpose; it's simply disregarded. For example, suppose you pay an invoice but fail to record the payment. Or you buy a tablet but fail to record it in your accounting system. This is readily accomplished if you misplace documents, such as a receipt or invoice, so that it is never documented.

3. Commission Error

This is mishandling an item by putting it in the incorrect accounting head. You enter the correct amount and even put it in the correct general account, but you then utilize the erroneous sub-account. For example, you may receive payment on an invoice but record the amount against another customer's invoice. Your overall payments are correct for accounting purposes, but what is displayed for a specific customer is incorrect.

4. Transposition Error

This error is caused by reversing numbers and registering the erroneous amount of an item. As a result of transposing a number, this can result in overstating or misunderstanding the amount of an item. For instance, instead of recording an expense as Rs.946, you enter it incorrectly as Rs.496. An error like this can be costly if a deductible amount is not claimed as a result of the entry error.

5. Compensating Error

This error is actually two errors that occur simultaneously; one offsets the other. It is difficult to detect because the net effect is zero. For example, you exaggerate your income by Rs.1,000 but understate your expenses by the same amount, so everything balances out even if both entries are incorrect.

6. Duplication Error

This happens when you enter the identical item of revenue or expense many times. Such an error can occur, for example, when multiple people have access to the accounting system and each enters the same entry.

7. Principle Error

This mistake occurs when an item is recorded that does not comply with Generally Accepted Accounting Principles (GAAP). This usually occurs when an entry is made in the incorrect account. The sum is right, but it is entered incorrectly. A principle error is a major procedural blunder since it can have serious implications. The most prevalent basic error is classifying an owner's personal spend as a business expense.

8. Error of Entry Reversal

This occurs when an expense is treated as an item of revenue or vice versa. You recorded a Rs.250 invoice in your accounts payable instead of your accounts receivable (i.e., you record it as an expense).

9.Closing Errors

Closing errors occur when accounts are not properly closed at the end of an accounting period. This may result in misstated profits or losses, erroneous financial statements and issues in subsequent reporting cycles. Appropriate year-end practices are necessary to prevent these disparities.

10.Reconciliation Errors

Reconciliation errors happen when recorded transactions do not match actual account balances, often due too missions, duplications, or incorrect entries. These errors can compromise financial accuracy and delay reporting, making regular bank and ledger reconciliations critical.

11.Misuse of Accounting Software

Misuse of accounting software, whether due to improper data entry, insufficient training, or incorrect settings, can lead to significant errors. These mistakes often result in inaccurate financial reports, hampering a company’s ability to track its financial health. Regular software audits and proper training are key to minimizing these errors.

How Accounting Errors affect business?

We understand that accounting errors in business can happen, whether they are small oversights or larger mistakes. However, even minor accounting errors can have a significant impact on a company’s financial health if not caught and addressed quickly.

Accounting errors can be trivial or major. They can have catastrophic repercussions in either case:

- Incorrect Income Reporting. Incorrect expense reporting might alter a company's computed operating profit margins or result in income overstatement.

- Incorrect Cash Flow Information. If things are not recorded correctly, the amount of cash on hand to pay bills may be overstated or understated.

- Incorrect Expense Reporting. Omission to declare a deductible item may occur from misclassification or failure to include business expenses. It may result in overpayment of taxes.

- Increased Labor Costs. Correcting classification errors on the back end takes time away from personnel who are already swamped with year-end reporting.

- Late Payment Fees. Invoices may become past due if misclassification errors are detected later in the accounting cycle, resulting in additional penalties and interest.

- Improper matching of Income and Expenses. Misclassified expenses may result in inaccurate reporting for organizations that employ accrual accounting. Expenses should be proportionate to the income generated. This will not occur if expenses are categorized in the incorrect month or year.

- Detecting Fraud. Employee fraud, including embezzlement, can occur in any firm, which is sad. When items do not match, it can suggest that something is wrong and that further inquiry is necessary

How to prevent Accounting Errors?

To prevent accounting errors, it is essential to be proactive and cautious with your financial information. How to avoid accounting errors starts with careful attention to detail, ensuring that each transaction is correctly recorded.

The first line of defense in ensuring that products are properly categorized and placed on your records is to be cautious with your financial information. Here are some procedures you may take to ensure accurate accounting entries.

1. Providing Training to the Staff

Make certain that staff who enter expenses into your accounting system are familiar with your accounts and descriptions. Give your system a thorough explanation. Take advantage of employee training provided by some software.

Establish a company policy for documentation procedures so that entries can be completed correctly and accurately. For example, keep track of employee reimbursements after they've completed expense reports so you know the figures are correct.

2. Employee Work Balance

Employees who are overburdened with work are more likely to make basic input errors than if they are given enough time to complete this activity. However, it is critical that your accounting is kept up to date and that you do not fall behind. Consider using expense report software to effortlessly import data into your accounting system to simplify and improve data entry and eliminate errors.

3. Upgrade Accounting Software

Use the most recent version of your accounting software. To ease the entire accounting process, software and cloud versions are constantly being enhanced. Cloud-based systems automatically update, but desktop software must be purchased every few years to stay current.

4. Implement Internal controls

Set up procedures to aid in the detection and correction of accounting problems. For example, perform bank reconciliations every a month to discover errors and keep them off your books. Credit card statements are the same way. Examine them on a monthly basis to check that charges have been put appropriately into your accounting system.

5. Check for differences between the budget and actual expenses

Use your accounting system to stay on track financially. Your budget may indicate that a specific amount of money is to be spent on a specific item or activity, but the entry does not match. A misclassification might be discovered by comparing your actual spending to the amount you budgeted (or at least an explanation for the differences).

6. Periodic Review of Accounts by Senior

You may wish to have your accountant review your accounts on a regular basis to ensure that they accurately reflect your spending and conform with GAAP. Your accounting software may provide a feature that allows your accountant to easily review customer data.

7. Adopt Best Accounting practices and standards

Don't let your employees procrastinate. Set deadlines for data entry and reconciliation so that mistakes are discovered immediately and readily fixed.

Conclusion

Understanding and preventing common accounting errors is essential for maintaining financial integrity and ensuring long-term business success. By staying vigilant and proactive, companies can avoid costly accounting mistakes that impact their financial health and operations. For businesses seeking expert support, Jordensky offers comprehensive solutions across accounting, tax, and CFO services, helping organizations build a strong financial foundation. Whether you need reliable accounting services in Mumbai, expert accounting services in Bangalore, or customized accounting services in Pune, Jordensky provides customized support to meet your unique business needs. Partnering with professional accounting services not only safeguards your financial records but also paves the way for greater financial growth and success.

About Jordensky

At Jordensky, we are committed to providing an experience of the highest caliber while specializing in accounting, taxes, MIS, and CFO services for startups and expanding businesses.

When you work with Jordensky, you get a team of finance experts who take the finance work off your plate– ”so you can focus on your business.

Also, Read

Understand the Basics of Accounting terms

Understand the Difference between Balance Sheet and Profit & Loss Statement