Understanding New Income Tax Regime vs Old Income Tax Regime

The new income tax regime provide lower income tax rate, while the old regime provides taxpayers with several tax saving options.

In this article

As a salaried individual, you have to pay taxes on your income. In India, there are two income tax regimes- the old tax regime and the new tax regime. While the old regime of income tax has been prevalent for decades, the new regime has been introduced in recent years. If you are confused about which one to choose, then this blog will guide you through the pros and cons of each regime.

Introduction

Tax planning is an essential aspect of financial planning for salaried people. The Indian government has recently introduced a new income tax regime, which offers a lower income tax rate but eliminates many tax deductions and exemptions. In this blog, we will compare the old income tax regime and the new income tax regime and help salaried individuals make an informed choice.

New Income Tax Regime vs Old Income Tax Regime: The Differences

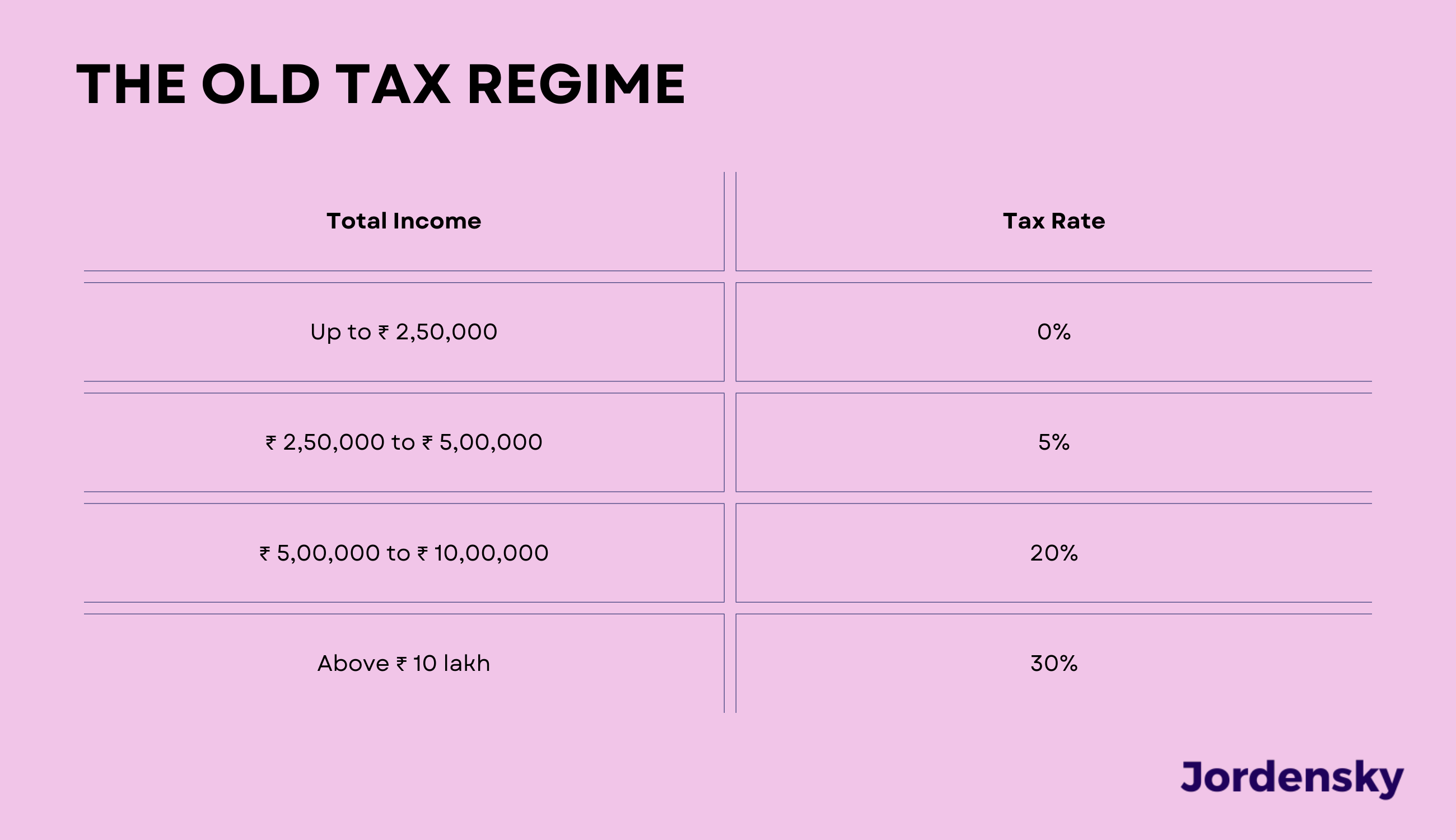

Old Income Tax Regime

Under the old income tax regime, taxpayers get to claim several tax deductions and exemptions such as HRA (House Rent Allowance), LTA (Leave Travel Allowance), standard deduction, and various investment options like PF (Provident Fund), PPF (Public Provident Fund), NSC (National Savings Certificate), and so on. However, under the new income tax regime, these deductions and exemptions are no longer applicable. Instead, taxpayers can enjoy lower income tax rates.

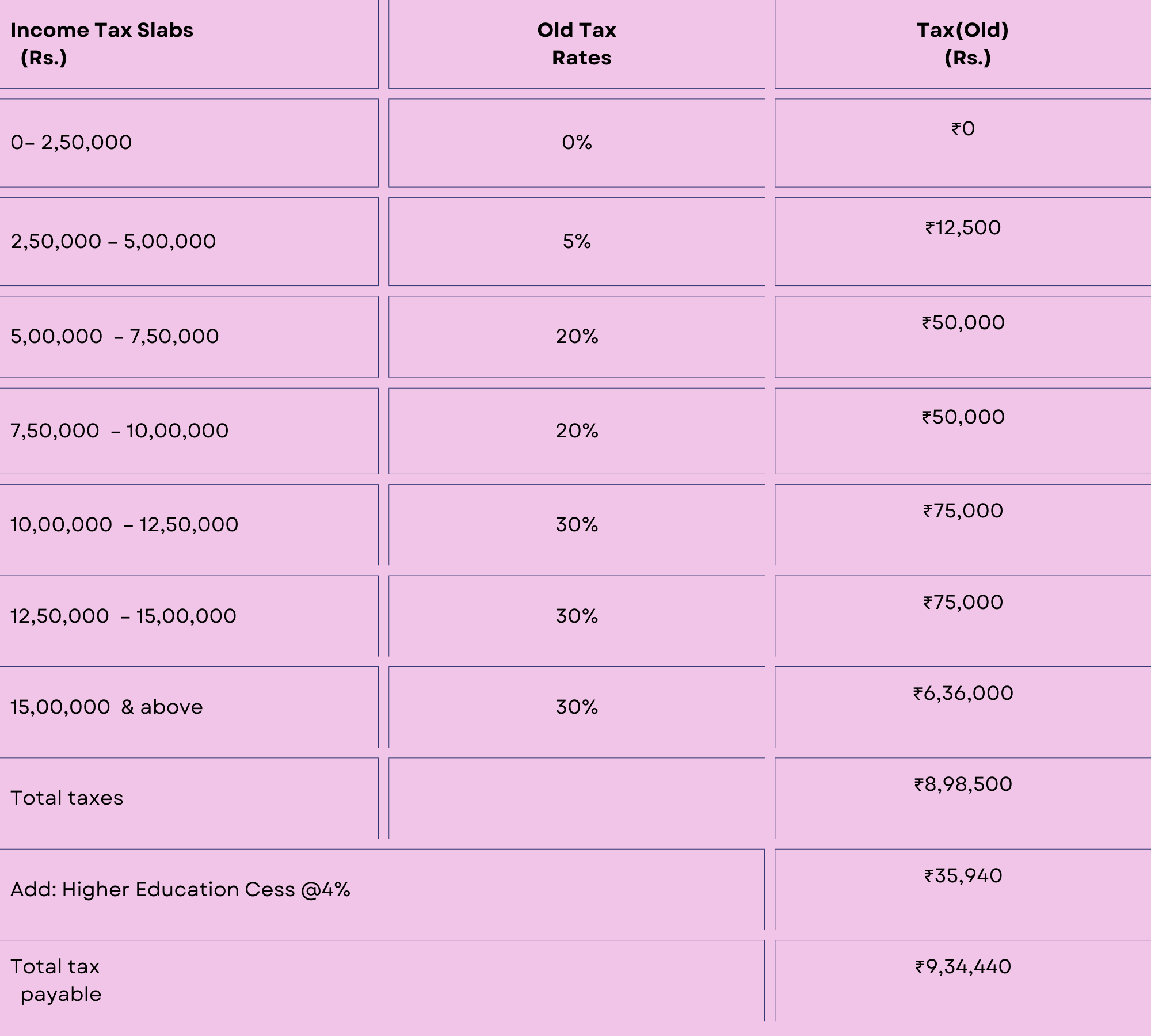

The income tax slabs were not tweaked for the old tax regime for FY24 and remain as below.

Choosing the old tax regime, on the other hand, permits you to claim a vast range of exemptions, some of which are stated below:

Income up to 1.5 lakh is exempt from tax under Section 80C of the Income Tax Act. This provides for the inclusion of pension funds (EPF, PPF), select mutual funds (ELSS), ULIPs, tax-saving fixed deposits, and other savings programmes such as National Savings Certificate, Sukanya Samriddhi Yojana, Senior Citizens Savings Scheme, and so on. Spending on life insurance, principal repayment on a home loan, or tuition for a kid can all qualify for Section 80C exemption.

Section 80CCD allows an additional 50,000 invested in NPS to be deducted from taxable income.

Other tax breaks, such as spending on health insurance for yourself and your parents, are allowable under Section 80D.

Other perks include leave travel allowance, house rent allowance based on wage structure and rent paid, and a variety of other exemptions that could be claimed under the previous tax regime.

The downside of the old tax regime is that the tax-saving options and deductions are challenging to keep track of, which can be time-consuming and tedious for individuals. Moreover, the taxable income is calculated based on the slab rate, and individuals have to pay a higher tax percentage based on their income bracket.

New Income Tax Regime

The new income tax regime offers lower income tax rates but comes with a caveat. To avail of this regime, the taxpayer must forego all tax deductions and exemptions, which tax-saving options. The principal advantage of the old regime is that taxpayers get to reduce their taxable income by claiming various deductions and exemptions. It translates into more significant savings in taxes for individuals with a higher income.

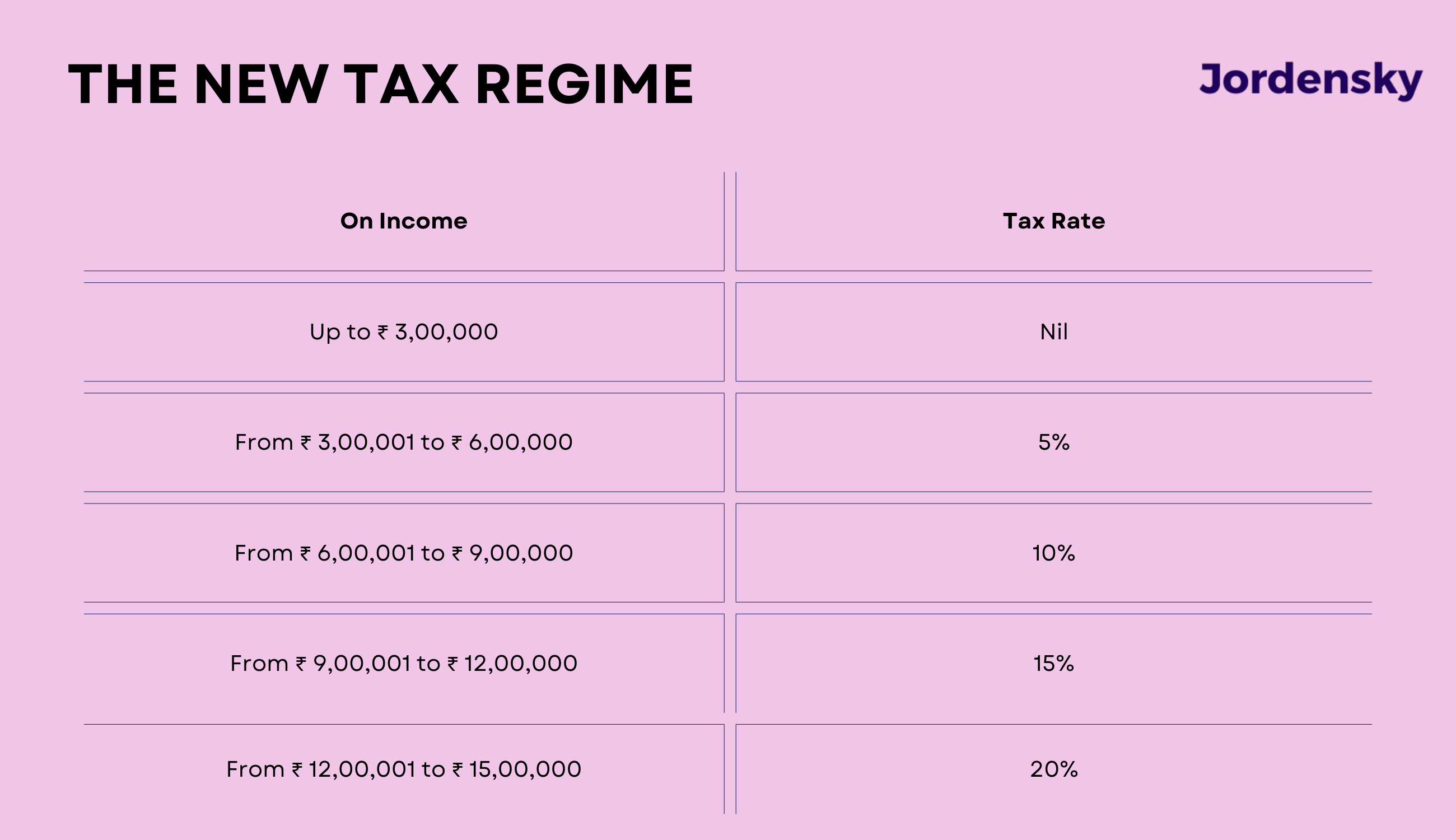

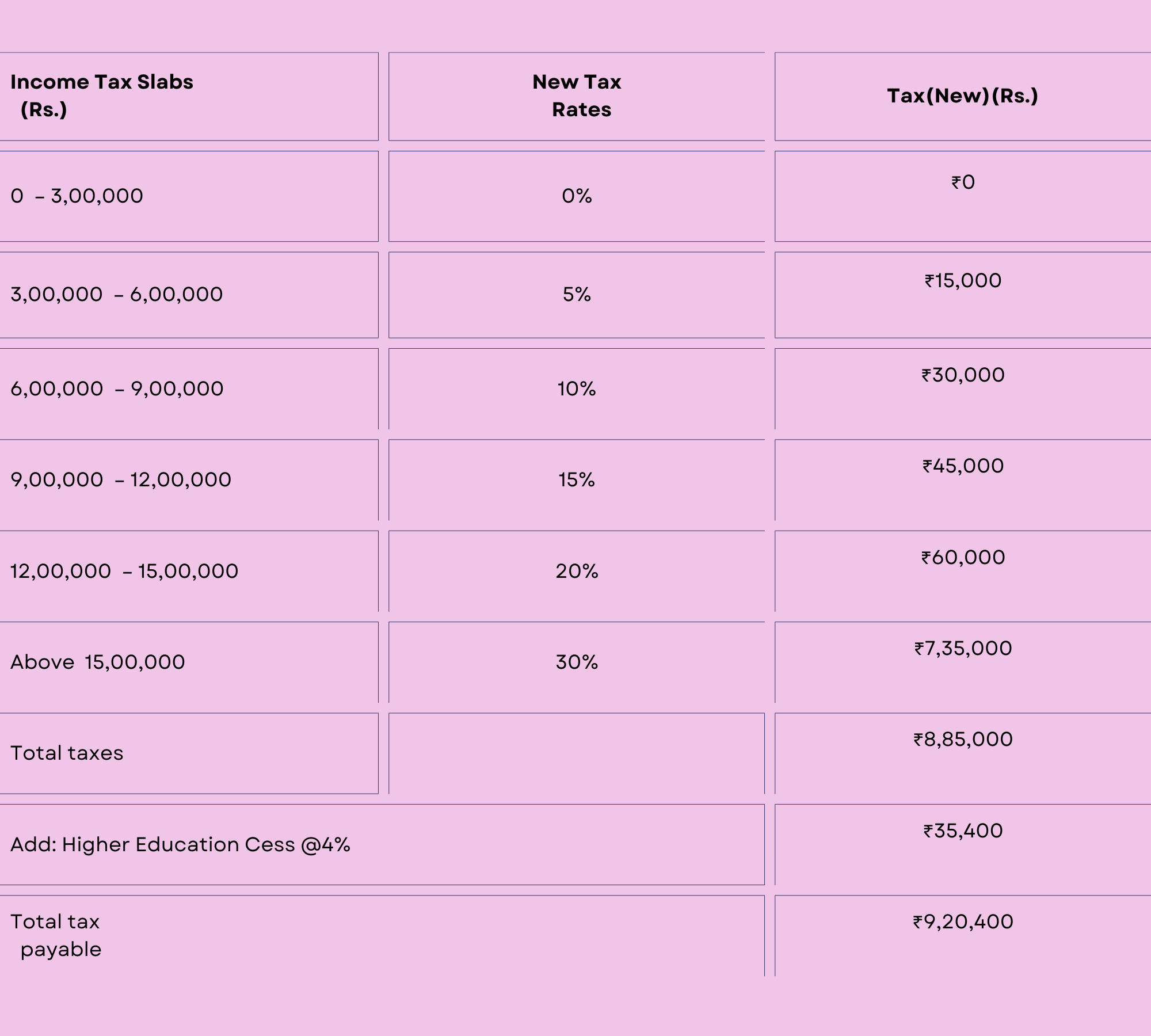

The income tax slabs for the new tax regime for FY24 are as below.

The new tax regime has six tax slabs, with 0% tax for income up to 3 lakh and a tax rate that rises by 5 percentage points for each additional 3 lakh of income.

Furthermore, the above tax rates apply to people with taxable income exceeding Rs. 7 lakh. According to the most recent declaration in the Union Budget 2023, persons with taxable income of less than 7 lakh will pay no tax.

Income tax is levied in progressive slabs. This means that if a person earns 10 lakh, they will not be paid a flat 15% rate on the full income (as shown in the chart above). In terms of taxation, their income up to Rs 3 lakh is tax-free, while income between Rs 3 lakh and Rs 6 lakh is taxed at 5% (i.e., 5% of Rs 3 lakh equals Rs 15,000). Income between 6 lakh and 9 lakh will be taxed at 10% (30,000), while the remaining 1 lakh will be taxed at 15% (15,000), bringing the total tax outlay to 60,000.

The new tax regime, like the old one, comes with one condition. The new tax regime, unlike the old tax regime, does not allow taxpayers to claim common exceptions. The FM did, however, declare that salaried taxpayers can deduct an additional Rs 50,000 from their income as a standard deduction for tax purposes.

Schedule call with Jordensky Tax Experts to understand which tax option is beneficial for you

Which is Better - Old vs New Tax Regime ?

Both the new and old income tax brackets have advantages and disadvantages. It all depends on whether or not you wish to claim deductions and exemptions under the new tax slab, which has a range of income levels and rates. The previous tax slab allows for deductions and exemptions. You should do a comparison examination and assessment under both tax systems before submitting your taxes.

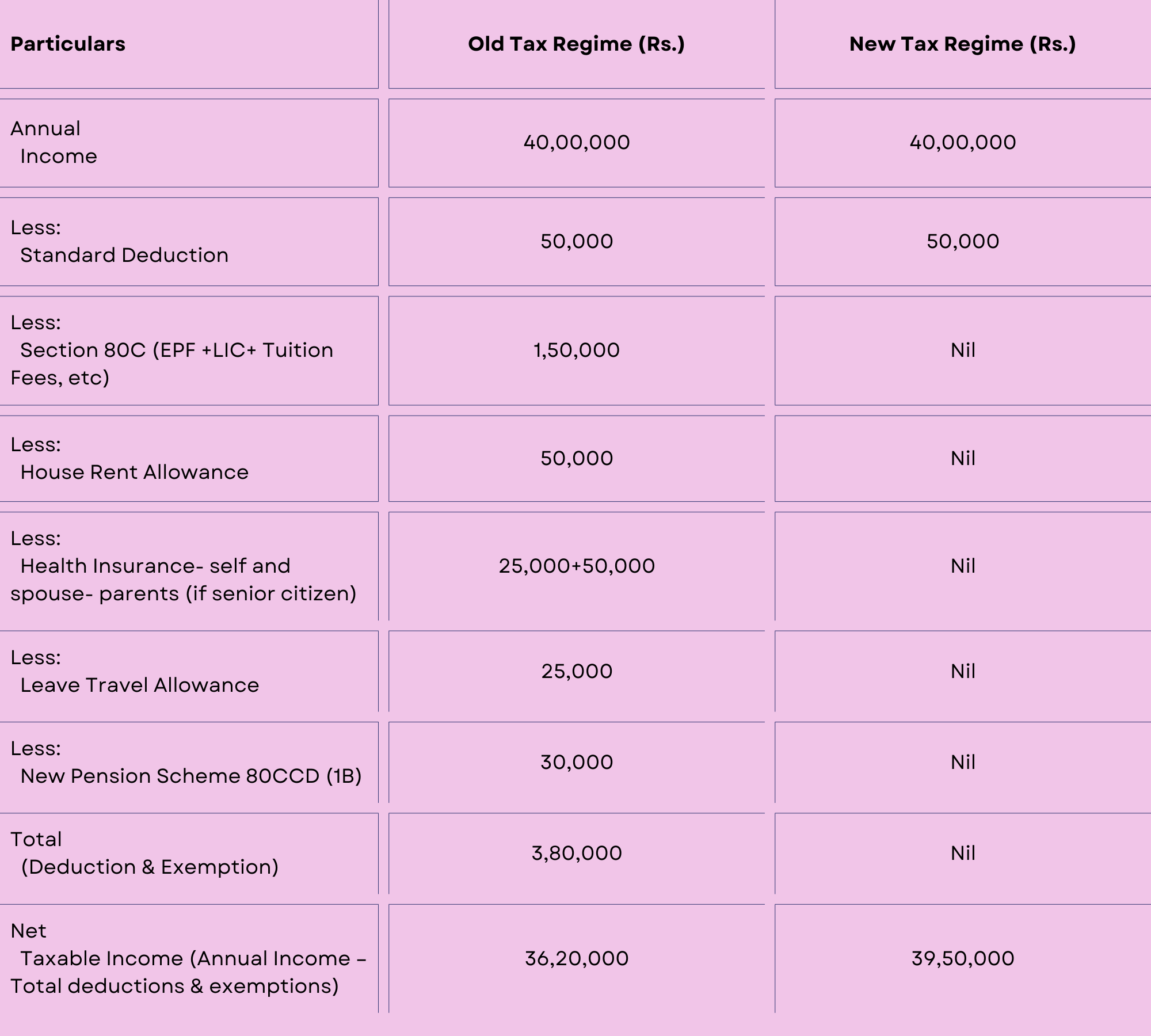

Let's take the case of Mr. Suresh, who earns Rs 40 lakh each year. The HRA deduction is Rs 50,000 per year. He makes use of the Section 80C ceiling of Rs. 1.5 lakh by combining EPF and ELSS mutual funds. He also got health insurance for Rs. 25,000 (self and spouse) and Rs. 50,000 (senior citizen - parents), which he claims as a tax deduction under Section 80D. He then put an extra Rs 30,000 into NPS to save even more taxes on his earnings. Suresh also claimed a Rs 25,000 tax-free Leave Travel Allowance.

Let’s see if the old vs new tax regime- which will put more money in his pocket.

Illustration on (Old vs New Tax Regime)

Total Tax Payable as per Old Regime

Total Tax Payable as per New Regime (FY 23-24 & AY 24-25)

So, as you can see, the new tax structure is superior. By choosing the new tax regime over the old, you will save Rs 14,040 in taxes.

Pros and Cons of New Income Tax Regime

The new income tax regime suits individuals who are not keen on dedicating enough time to plan their finances and consider tax-saving options. The income tax rates under the new regime are lower than the old regime, and simpler to calculate. It saves taxpayers plenty of time and hassle.

However, the new regime comes with its disadvantages as well. The lack of deductions and exemptions means that the taxable income is higher for individuals with significant investments and deductions. The taxpayers saving on taxes under the new regime may end up using these savings to pay more for other features like higher medical expenses

Pros and Cons of Old Income Tax Regime

The old income tax regime may not be suitable for everyone, but it has its advantages for people who are willing to plan their finances and invest in a smart manner.

Under the old regime, taxpayers have the option to choose between a deductions-based structure and a flat tax rate structure. For those who know how to maximize their deductions or have made significant investments, this can translate to significant savings on their tax bill. However, it is important to note that the old regime comes with fewer tax exemptions and rebates, and it is important to assess one's financial situation before committing to it.

For those looking to make the most of their finances, the old income tax regime remains a viable option.

Conclusion

The new income tax regime has its advantages, like the lower income tax rate, while the old regime provides taxpayers with several tax-saving options and exemptions. So which regime is better suited for you? It all depends on individual preferences, spending, and investment patterns. We recommend that you evaluate both regimes' pros and cons and choose the one that aligns with your financial goals and long-term savings plan.

Reader's key action: We encourage you to consult a financial advisor and evaluate both regimes' benefits and drawbacks before making any decisions. Schedule call with Jordensky Tax Experts to understand which tax option is beneficial for you