Cancellation, Revocation and Re-registration Process under GST

Detailed Process on Cancellation, Revocation and Re-registration under GST Act

.png)

In this article

How to Cancel, Revoke, and Re-Register under GST?

If businesses exceed the yearly turnover thresholds, each person and every company must register for the Goods and Services Tax (GST).Similar to this, registration is mandatory for anyone making an inter-state taxable supply of goods or services. The taxpayer can also request that an officer cancel their GST registration if they are no longer needed to pay tax. There can be no supply of goods and services unless the cancellation is over turned. So let's learn more in this post about the cancellation of a GST registration, how to reactivate a GST number, and other relevant information.

Cancellation of GST Registration

The cancellation of the taxpayer's GST registration results in their termination as a GST registered person. They won't have to submit GST returns because they won't have to pay or collect GST or make any claims for input tax credits.

In accordance with Section 29 of the CGST Act and Rules 20, 21,and 21A of the 2017 CGST Rules, there is an option for cancellation.

Types of Cancellation under CGST Act,2017

- On Request of Taxpayers

- By Tax Officer Order

- Request by legal heirs, in case of death of the taxpayer

How to surrender GST number?

- There are two ways for taxpayers to withdraw their GST numbers:

- Cancellation of Migrated Tax Payers GSTIN(Goods and Services Tax Identification Number)

- Other Cancellation by Taxpayers

Also Read: Registration Of GST

Cancellation of Migrated Tax Payers GSTIN

Individuals enrolled under the previous indirect tax system would be required to switch to the GST. Many of these individuals might not need to register for GST. However, they are unable to produce interstate goods because all interstate suppliers—aside from service providers—are required to register.

Such a taxpayer shall make an electronic application in Form GST REG-29.

The appropriate officer will terminate the registration after conducting the necessary inquiry.

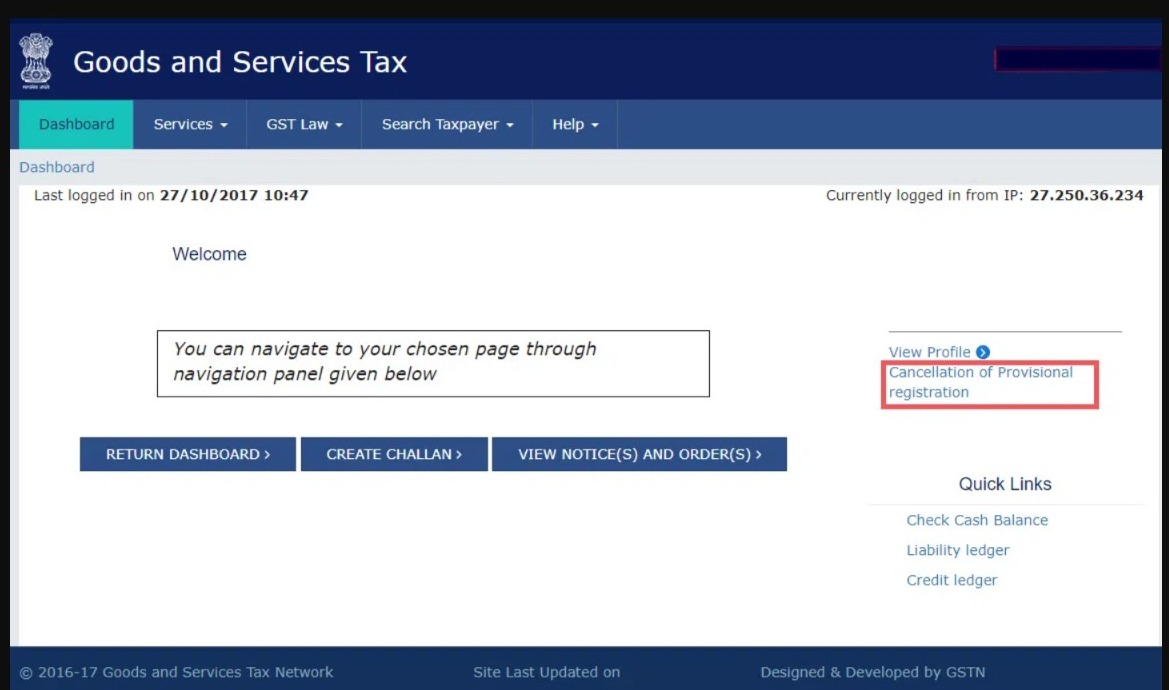

Following are the actions that migrating taxpayers must take in order to cancel their GSTIN on the GST Portal:

Step 1:

Select Cancellation of Provisional Registration from the drop-down menu after logging into the GST Portal(gst.gov.in).

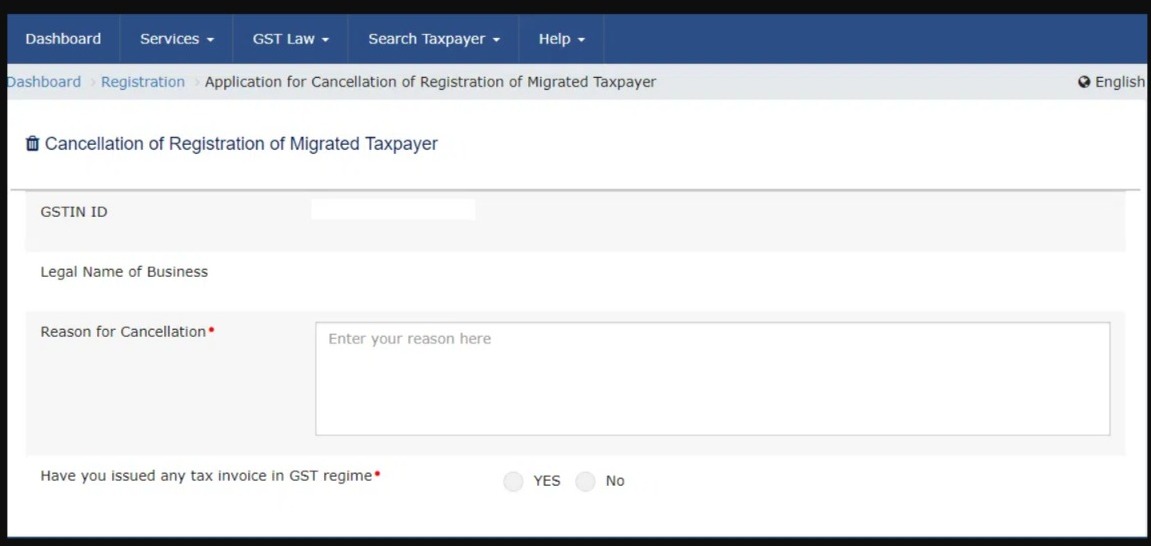

Step 2:

- The Cancellation Page is now open.

- Your GST Registration Number and Name of Legal Business will show automatically.

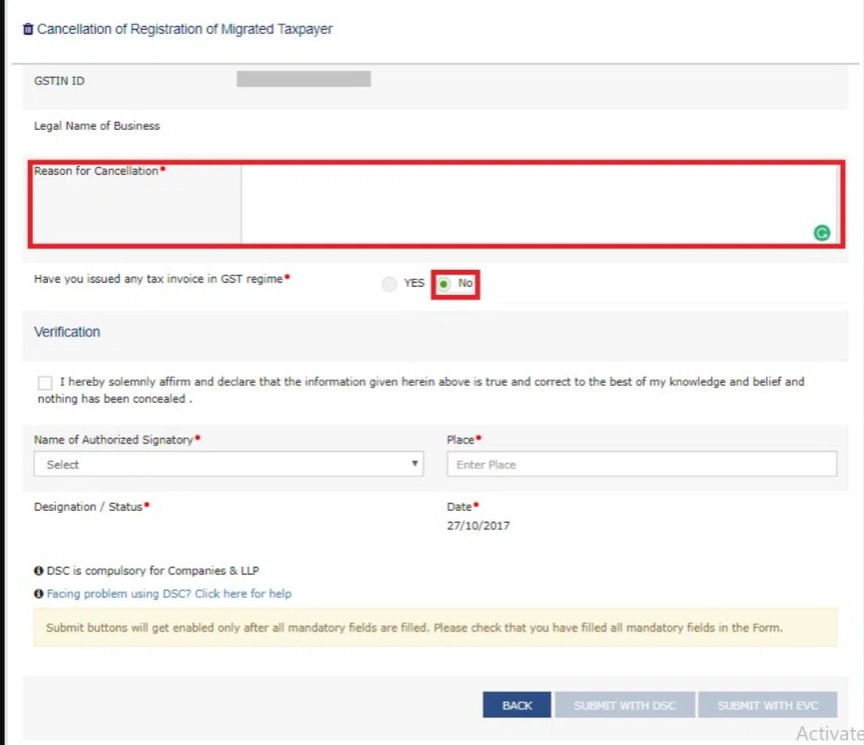

- Now, you are required to give a Cancellation Reason.

Note: If you have issued any tax invoices throughout the month, you will be required to provide that information.

Enter the data for the authorized signatories, then submit. If you're a sole proprietorship or partnership, sign off by entering the Electronic Verification Code (EVC). For LLPs and businesses, a digital signature certificate (DSC) is a requirement.

Cancellation by Taxpayers- Other Reasons

Why would a taxpayer decide to discontinue their GST registration?

- The business of the taxpayer has been completely transferred, amalgamated, demerged, or otherwise disposed of.

- The transferee (or the new business created as a result of the merger or demerger) must register. The registration will be cancelled if the transferor closes its doors.

- The company's constitution has been modified.

The taxpayer must use the GST Portal to make an electronic application in FORM GST REG-29 for cancellation. An authorized authority will cancel the registration following a thorough examination.

If a registered person's registration is cancelled, they must file a final return within three months of the cancellation date or the date of the cancellation order, whichever is later, unless they are an Input Service Distributor, a non-resident taxable person, or a person paying tax under the composition scheme or TDS/TCS. Either directly through the common portal or a Facilitation Center approved by the Commissioner, it must be submitted electronically in FORM GSTR-10.

For Example,

1) Private Limited is changed to a Public Company.

2) Sole Proprietor has changed to Partnership Firm or LLP as the case may be.

Cancellation by Tax Officer- Proper Officer

A proper officer may remove the taxpayer's registration number for the following reasons:

- The registrant doesn't conduct business from the address they gave when registering.

- Even though no products or services have been supplied, the registered person nevertheless sends out bills.

- The registered person disobeys the law against profiting

- ITC from their electronic credit ledger may be used by taxpayers who breach Rule 86B and have a total taxable value of supply that exceeds 50 lakh in a month to discharge more than 99 percent of their tax liability.

- involves using the input tax credit in violation of Section 16 of the Act or the rules

- A taxpayer has neglected to submit GSTR-3B for more than six months.

- If there are Significant Anomalies" between the values of outward supplies documented in GSTR3B and those revealed in GSTR1 ITC, the suspension will be triggered. Compared to GSTR 2B accessible values, GSTR 3B declared value.

GST Cancellation Process

Cancelling the GSTIN: The following actions must be taken by the Authorized Person, or Proper Officer:

- In Form GST REG 17, a show-cause notice (SCN) is delivered to the authorized person.

- Within seven days of receiving the notice, the registered person must reply in FORM GST REG -18 if there is a dispute.

- The authorized official may dismiss the case and issue an order in FORM GST REG-20 if they are pleased with the submission.

- If the registered individual fails to provide a defense as to why their registration should not be cancelled, the authorized officer will issue an order in Form GST REG-19.

- Within 30 days after receiving the show-cause notice, the order will be delivered.

Cancellation by Taxpayers Legal Heirs

- When a registered person passes away, their family or legal successors may revoke their GST registration by completing Form GST REG 16.

- Details about inputs, semi-finished goods, and finished goods held in stock on the date of cancellation of registration must be included in Form GST REG 16 by the legal heirs.

- Liability, if any

Process for Cancelling a GSTIN

According to CGST Act2017 Rule-22, the following steps must be taken to cancel a GSTIN:

- The registered person may apply for cancellation or the proper officer may act on their own.

- The registration may be revoked backwards in cases of fraud, deliberate misrepresentation, or omission of information.

- Tax obligations that were accumulated prior to the cancellation date would not be impacted.

- A notice of the hearing and the chance is given prior to cancellation.

The voluntary submission of GST number procedure

The information on the inputs, semi-finished items, and finished goods in stock, as well as any liabilities or pending payments, must be included in the application submitted in Form REG 16.

If a person who has requested the cancellation of his registration is no longer eligible to be registered or if his registration is eligible to be cancelled, the relevant official must issue an order in Form GST REG-19 within thirty days of the date of the application.

After submitting an application for cancellation of registration in FORM GST REG-16, the status of the GSTIN will be changed to "Suspended" until the PO issues the final order of cancellation.

- In case of reasons to believe with the proper officer that GST registration of the taxpayer should be cancelled suo moto, he shall issue a notice in Form REG 17 requiring the taxpayer to show cause why his no. should not be cancelled.

- The reply to Show Cause Notice (SCN) has to be submitted by the taxpayer by GST REG 18 within the time specified.

- After consideration of REG18, the Proper officer decides that the taxpayer is no longer liable to be registered .They may cancel their registration, issue an order in REG 19 and direct them to pay any due within

Suo Moto Cancellation procedure

Revocation of GST Registration Number Cancellation

The GST Act is fairly comprehensive and contains clauses and guidelines that cover a variety of potential scenarios that a taxpayer might run across. The procedure for revoking a GST registration cancellation order and the necessary forms are covered in the section that follows. The provision for revocation is found in Rule 23 of the CGST Rules, 2017.

Revocation Time Period

Any registered taxable person may request the revocation of the cancellation of their GST registration within 30 days of the day the order to that effect was served. It should be emphasized that only if the appropriate authority has cancelled the registration on their own initiative may an application for revocation be lodged. Therefore, when taxpayers voluntarily terminate their GST registration, revocation cannot be used.

Revocation Process

The registered individual must submit FORM GST REG-21, either directly or through a facilitation center chosen by the Commissioner, in order to request the cancellation of their GST registration.

Online Registration Cancellation Revocation Process on the GST Portal

- To access the GST Portal, go to gst.gov.in.

- To access the account, type the username and password.

- Choose registration from the services option under the GST Dashboard, then services, registration, and finally an application to revoke a cancelled registration under registration.

- In the select box, type the justification for the revocation of the cancellation. Additionally, you need to fill out the form, check the verification box, choose the name of the authorized signatory, and choose the appropriate file to attach for any supporting documents.

- The last step is to check the boxes for DSC or EVC submission.

Application for Revocation Processing

The cancellation of registration will be revoked by the proper officer if the taxpayer's justification for doing so is accepted by the official.

The license can be revoked by the officer 30 days after the application date. The appropriate officer must issue an order restoring the cancellation of registration in FORM GST REG-22.

Application for Revocation Rejected

A notification in FORM GST REG-23 will be sent if a Proper Officer is not satisfied with the revocation application. The applicant must provide a complete response in FORM GST REG-24 within 7 working days after the day the notification was served. The officer must issue a pertinent order in FORM GSTREG-05 within 30 days after obtaining a satisfactory response from the applicant after receiving that response.

Re-Registration of GST after Cancellation under CGST Act, 2017

Any seller of taxable goods and services that exceeds the threshold threshold must register for GST, as was previously stated. However, recent petitions for new registration of businesses whose registrations had been revoked by an inspector for failing to comply with statutory requirements have been received by GST officials.

On March28, 2019, the Central Board of Indirect Taxes and Customs (CBIC) released Circular No. 95/14/2019-GST, in which officials outlined the repercussions that the taxpayer will experience if the cancelled registration is not revoked.

The authorized officer must ascertain whether any prior registrations existed and whether they were revoked when a registered taxpayer requests a new registration within the same state.

The application for re-registration of GST after Cancellation may be rejected, and the taxpayer may be asked to file all outstanding returns first. If the earlier registration is cancelled, the next step is to determine whether the cancellation was caused by a violation of section 29 (2) (b) [composition dealer has not filed returns for three consecutive tax periods] or section 29(2) (c] [registered taxpayer has not filed returns for a continuous period of six months]. The Form GST REG-21 must be submitted in order to re-register.

Important Information: Extension of the Revocation Date

The deadline for making an application for the revocation of cancellation of registration falls between the first of March 2020 and the last day of August 2021, although the time limit for doing so has been extended to the 30th of September 2021. The Central Board of Indirect Taxes & Customs (CBIC) has mandated that Aadhaar authentication be required for the revocation or cancellation of GST registration beginning in January 2022.

Conclusion

Understanding the process for cancelling registration by the taxpayer and the authorities is crucial. There are a total of two ways for taxpayers to cancel their taxes. Additionally, the proper officer or the taxpayer's legal heir may execute the cancellation. If you want to renew a cancelled GST registration, you can do so by going through the re-registration process. We trust that this article has given you comprehensive knowledge of the regulations governing GST registration cancellation, revocation, and re-registration under the GST Act.

About Jordensky

At Jordensky, we specialize in accounting, taxes, MIS, and CFO services for Startups and growing business and are focused on delivering an experience of unparalleled quality.

When you work with Jordensky, you get a team of finance experts who take the finance work off your plate – ”so you can focus on your business.