Section 194C of the Income Tax Act

Section 194C provides for deduction of tax at source from the payment made to resident contractors and sub-contractors.

According to Section 194C of the Income Tax Act, TDS must be withheld from any payments made to a resident who is performing "work" under the terms of a contract between the "specified person" and the resident contractor.

The term "specified person" as used above refers to:

- The Central Government or any State Government; or

- Any local authority; or

- Any statutory corporation; or

- Any company; or

- Any co-operative society; or

- Any statutory authority dealing with housing accommodation; or

- Any society registered under the Societies Registration Act, 1860; or

- Any trust; or

- Any university established under a Central, State or Provincial Act and an institution declared to be a university under the UGC Act, 1956; or

- Any firm; or

- Any Government of a foreign State or foreign enterprise or any association or body established outside India; or

- Any person, being an individual, HUF, AOP or BOI, who has total sales, gross receipts or turnover from the business or profession carried on by him exceeding Rs.1 crore in case of business and Rs.50 lakhs in case of profession during the financial year immediately preceding the financial year in which such sum is credited or paid to the account of the contractor.

It should also be noted that the phrase "contract" covers "sub-contract."

The term ‘work’ includes the following:

- Advertising;

- Carriage of goods / passengers by any mode of transport except railway;

- Broadcasting and telecasting (which also includes the production of programmes for such broadcasting or telecasting);

- Catering;

- Manufacturing / supplying a product based on the requirement and specification of customers by using material purchased from the customer. However, it doesn’t include when the material is purchased from any person other than the customer.

List of exceptions or instances where TDS is not required to be deducted under Section 194C of Income Tax

TDS is not required to be deducted in the following situations:

- The amount paid or credited to the contractor in a single invoice / bill doesn’t exceed INR 30,000.

- The aggregate amount paid or credited during the financial year doesn’t exceed INR 1,00,000.

- The amount paid / credited to the account of the contractor engaged in the business of hiring, plying or leasing goods carriage, where the contractor doesn’t own more than 10 goods carriage at any time during the previous year. The Contractor is required to furnish the declaration along with the PAN to the deductor.

- The amount is paid or credited to the contractor by an individual / HUF for carrying out work in the nature of personal use.

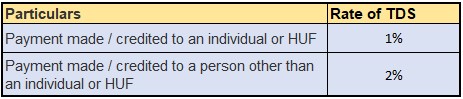

Rate of TDS under section 194C

The applicable rates of TDS under section 194C are as follows –

However, if the PAN is not provided, the Deductor will be required to deduct TDS at the highest marginal rate of 20%.

Time of TDS deduction under Section 194C

If the terms of Section 194C of the Income Tax Act require the Deductor to deduct TDS, the Deductor must do so by the earliest of the dates listed below.

- At the time of credit of sum to the account of the Contractor; or

- At the time of payment in cash or cheque or draft or any other mode.

Due date for TDS deposit / payment under Section 194C

Due Date of Issuance of TDS certificate u/s 194C

- April to June - 15th August

- July to September - 15th November

- October to December - 15th February

- January to March - 15th June

Rules for Filing Returns under Section 194C

Every Deductor required to deduct TDS pursuant to Section 194C is required to submit a quarterly return in Form 26Q by the deadlines listed below:

- April to June - 31st July

- July to September - 31st October

- October to December - 31st January

- January to March - 31st May

FAQ's on TDS under Section 194C

Que 1. Do sales marketing expenses qualify for TDS deductions?

Yes, TDS is deductible on Sales and Marketing expenses. Sales promotion costs may be incurred in place of contracts or as compensation for expert services. TDS will be relevant in both situations even if there are different section of TDS that apply.

Que 2. Is a written contract required in order to be eligible for the TDS under Section 194C?

No. A formal contract is not always required to trigger section 194C. TDS may be deducted even if an agreement was just verbal.

Que 3. Should the gross amount or the net amount including GST be used to calculate the TDS under section 194C?

TDS must be subtracted from the invoice amount before any additional taxes, such as GST

Que 4. What justifies the deduction of TDS?

The TDS method enables the government to receive payments on a constant basis. In addition, TDS makes it easy to trace revenue and also helps to prevent tax avoidance.

About Jordensky

At Jordensky, we are committed to providing an experience of the highest caliber while specializing in accounting, taxes, MIS, and CFO services for startups and expanding businesses.

When you work with Jordensky, you get a team of finance experts who take the finance work off your plate– ”so you can focus on your business.

.png)