How to Setup Business in India: 2026 Guide for Foreign Firms

Foreign company entering India in 2026? Compare entry routes, FDI rules, taxes, and timelines in one CFO-level guide.

Table of Contents

Subscribe to our Newsletter

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

India is the fastest-growing major economy in 2026 — and the most misunderstood market that foreign companies try to enter. Founders arrive expecting speed. They leave understanding structure. The companies that win in India spend their first 90 days getting three things right: the right India entry vehicle, the right FDI route, and the right tax and transfer-pricing process. The companies that struggle do the opposite — they incorporate first and ask questions later.

This is the CFO-level guide we walk every foreign companies through before they spend on incorporation. You'll get the entry-vehicle comparison, the FDI automatic-vs-approval map, the step-by-step incorporation timeline, cost benchmarks, the compliance calendar, and the 10 mistakes that cost foreign companies the most. By the end, you'll know exactly which India structure fits your business — and why.

How a Setup a Foreign Company in India

For most foreign companies entering India in 2026, the process looks like this:

Choose an entry vehicle — a wholly-owned subsidiary (Pvt Ltd) is the default for 80%+ of cases.

Confirm the FDI route — automatic (most sectors) or government approval (defence, telecom, media, etc.).

Incorporate the company— Reserve the name, file SPICe+, and obtain CIN, PAN, TAN, GST, and IEC.

Open a Bank account and infuse share capital from the foreign parent.

Comply with FEMA — File FC-GPR within 30 days of share allotment.

Set up tax, payroll, and statutory compliance — income tax, GST, TDS, PF/ESI, and shops & establishments.

Plan transfer pricing before the first intercompany transaction.

End-to-end timeline: 3–6 weeks if your structure is straightforward, 8–12 weeks with regulatory approvals.

Why India Matters for Foreign Companies in 2026

Three trends are pulling foreign capital and operations into India faster than ever:

The world's largest English-speaking talent pool in tech, finance, and operations — at 30–60% of the cost of Western markets.

A digital infrastructure stack (UPI, Aadhaar, GST, DigiLocker) that no other emerging market has matched.

Production-Linked Incentives (PLI), GIFT City, and a maturing FDI regime that have made India a "China-plus-one" default for global supply chains.

The flip side: India rewards companies that respect structure. The penalties for getting FEMA, transfer pricing, or GST wrong are real — interest, prosecution, and, in extreme cases, restrictions on remittances. A clean entry plan saves you 18–24 months of pain.

The default. A separate legal entity owned 100% by the foreign parent (or 99.99% + 0.01% with a nominee, since a Pvt. Ltd needs 2 shareholders). Best for full operations, hiring, revenue, and long-term presence. Covered by our Private Limited Registration Process in India: Step-by-Step Guide.

Limited Liability Partnership (LLP)

Hybrid structure. Lighter compliance than a Pvt. Ltd, but FDI in LLPs is allowed only in sectors with a 100% automatic route. Suitable for professional services and consulting; not ideal for VC-backed structures.

Liaison Office (LO)

A representation-only office. Cannot earn revenue, cannot invoice, cannot trade. Allowed only for limited activities — market research, communication, brand building. Good for testing the market for 12–24 months.

Branch Office (BO)

Allowed for foreign companies engaged in manufacturing or trading abroad. Can earn revenue but with restrictions. Profits are taxed at the higher foreign-company rate of ~40%.

Project Office (PO)

Set up for executing a specific contract in India (often EPC, infrastructure). Auto-closes when the project ends.

Joint Venture (JV)

A separate Indian entity owned partly by the foreign parent and partly by an Indian partner. Used when sectoral caps require Indian ownership (e.g., insurance, defence, multi-brand retail) or when local distribution/regulatory expertise is essential.

Comparison of Various Entity Structure for India Entity Registrationn

Dimension

WOS (Pvt Ltd)

LLP

Liaison Office

Branch Office

Project Office

Joint Venture

Can earn revenue in India

✅ Yes

✅ Yes

❌ No

✅ Yes (restricted)

✅ Yes (project-only)

✅ Yes

Foreign ownership allowed

Up to 100%*

Up to 100%*

100%

100% (parent)

100% (parent)

Up to sector cap

Separate legal entity

✅ Yes

✅ Yes

❌ No (extension)

❌ No (extension)

❌ No (extension)

✅ Yes

Income tax rate (2026)

25.17% (incl. surcharge & cess)**

30%+

N/A (no income)

~43.68%

~43.68%

25.17%

Compliance burden

Medium–High

Low–Medium

Low

Medium

Low–Medium

Medium–High

Setup timeline

3–6 weeks

4–6 weeks

6–10 weeks (RBI)

6–10 weeks (RBI)

4–8 weeks (RBI)

6–12 weeks

Approval needed

Automatic in most sectors

Automatic in 100% sectors only

RBI approval

RBI approval

RBI approval

Sector-dependent

Best for

Long-term operations

Light-asset services

Market testing

Foreign trading firms

Specific contracts

Regulated sectors

*Subject to sector-specific FDI rules. **Concessional rate of 22% (effective 25.17%) under Section 115BAA, available to most domestic companies.

For 80%+ of foreign companies entering India in 2026, the wholly-owned subsidiary (Pvt. Ltd) is the right answer. Liaison and branch offices are increasingly rare.

FDI in India — Automatic vs Approval Route

India operates a two-track FDI regime, governed by FEMA, the FDI Policy (DPIIT), and the RBI:

Route

Description

Timeline

Automatic Route

No prior approval needed. File post-investment FC-GPR within 30 days of share allotment. Covers most sectors up to specified caps.

0 days (post-filing only)

Government Approval Route

Prior approval from the relevant ministry via the FIFP portal. Covers sensitive sectors.

Note: "Automatic route" doesn't mean "no compliance". It means no prior approval. Post-investment reporting (FC-GPR, FLA, ODI, etc.) is non-negotiable, and missed filings invite compounding penalties under FEMA.

Always check the current sectoral FDI cap on the officialDPIIT FDI Policy(dpiit.gov.in) and RBI FEMA Master Direction (rbi.org.in) before incorporating.

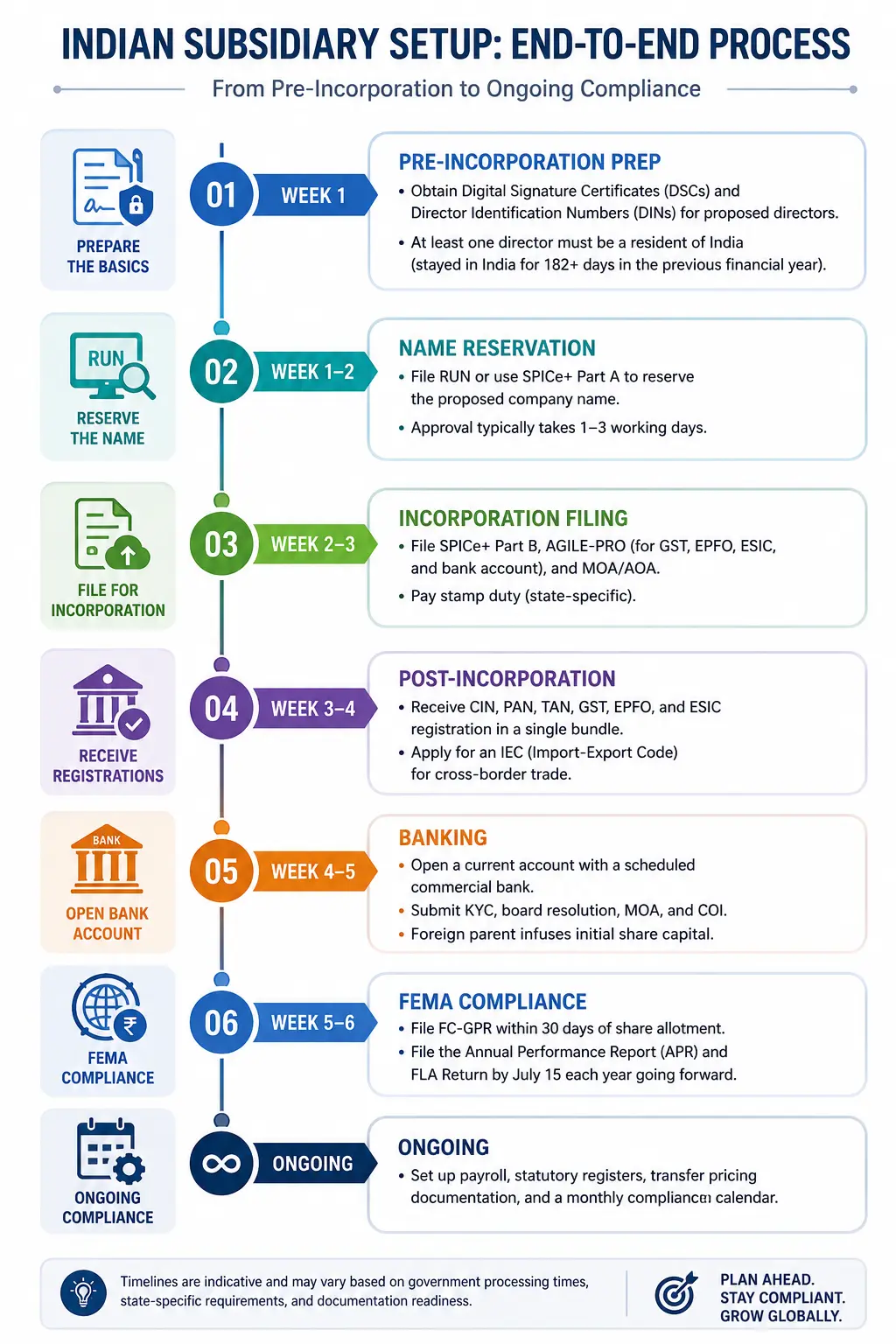

How to Incorporate a WOS in India — Step-by-Step

The cleanest 6-week path to a fully operational subsidiary:

Week 1: Pre-incorporation prep. Obtain Digital Signature Certificates (DSCs) and Director Identification Numbers (DINs) for proposed directors. At least one director must be a resident of India (stayed in India for 182+ days in the previous financial year).

Week 1–2: Name reservation. File RUN or use SPICe+ Part A to reserve the proposed company name. Approval typically takes 1–3 working days.

Week 2–3: Incorporation filing. File SPICe+ Part B, AGILE-PRO (for GST, EPFO, ESIC, and bank account), and MOA/AOA.. Pay stamp duty (state-specific).

Week 3–4: Post-incorporation. Receive CIN, PAN, TAN, GST, EPFO, and ESIC registration in a single bundle. Apply for an IEC (Import-Export Code) for cross-border trade.

Week 4–5: Banking. Open a current account with a scheduled commercial bank. Submit KYC, board resolution, MOA, and COI. Foreign parent infuses initial share capital.

Week 5–6: FEMA compliance. File FC-GPR within 30 days of share allotment. File the Annual Performance Report (APR) and FLA Return by July 15 each year going forward.

Ongoing: Set up payroll, statutory registers, transfer pricing documentation, and a monthly compliance calendar.

Tax & Compliance for Foreign Companies in India

This is where most foreign entrants underestimate complexity. The headline rates and obligations:

Tax / Compliance

Rate / Requirement (2026)

Frequency

Corporate income tax (domestic Pvt Ltd)

22% (effective ~25.17% with surcharge & cess) under Section 115BAA

Annual + advance tax (4 instalments)

Corporate tax (foreign company / branch)

35% + surcharge & cess (~38%–42% effective)

Annual + advance tax

Minimum Alternate Tax (MAT)

15% + surcharge & cess (where applicable)

Annual

Dividend Distribution

DDT abolished — dividends now taxed in shareholder's hands; TDS @ 20% (subject to DTAA)

PF 12%, ESI 3.25% (employer) — wage thresholds apply

Monthly

Transfer Pricing — Form 3CEB

Mandatory if any international related-party transaction

Annual

FEMA (FC-GPR, FLA, APR)

As per share/asset movements

Per event + annual

The transfer pricing piece deserves special attention: every related-party transaction (royalties, management fees, intra-group loans, IP licensing, and cost sharing) must be at arm's length, documented contemporaneously, and certified annually via Form 3CEB. Get this wrong and you invite a TP audit that takes 3–5 years to resolve.

These are realistic ranges from 100+ Indian entry engagements. Costs vary by city (Mumbai/Bangalore/Delhi NCR are 20–40% higher than Tier 2) and complexity (multi-state GST, transfer pricing, and FDI approvals).

Common Mistakes Foreign Companies Make while setting up India Entity

Choosing the wrong vehicle. Setting up a liaison office "to test the market" and then trying to invoice through it. You can't.

Ignoring transfer pricing on Day 1. Inter-company contracts written 18 months later don't survive a TP audit.

Underestimating GST. Multi-state operations create multi-state GST registrations. Plan for it.

Hiring before payroll setup. PF and ESI registrations must precede the first pay cheque.

Missing FC-GPR. A 30-day deadline. Late filing triggers FEMA compounding penalties (₹5K – several lakhs).

Using personal accounts for business expenses. Disqualifies expenses, triggers tax addition, and complicates the audit.

Sending the foreign CFO without an India tax advisor. Indian tax law is uniquely procedural. Even great global CFOs need local counsel.

Treating board meetings as optional. Pvt Ltds in India must hold at least 4 board meetings/year, with gaps ≤ 120 days. Missing this triggers ROC penalties.

No data localisation plan. Sectoral data localisation rules (RBI for payments, MeitY for personal data) catch many foreign companies off-guard.

Not appointing a resident director who is reachable. When the MCA/RBI sends a notice, someone in India must be able to act — fast.

Expert Tips for a Smooth India Entry

Map the next 24 months before incorporating. Will you hire engineers? Sell to enterprises? Import goods? Each path changes the optimal structure.

Pick a city deliberately. State-level stamp duty, professional tax, and labour law differ. Karnataka, Maharashtra, Telangana, and Haryana are popular choices for tech and services.

Build a 13-week cash flow before Day 1. Repatriation is structured, not free. Plan how money flows back.

Use one professional firm for compliance + one for transfer pricing. Don't fragment. Audits cross-reference everything.

Set up a board cadence in advance. A foreign parent representative and an India resident director are the minimum.

Document IP ownership clearly. Indian R&D done by an Indian subsidiary creates IP that must be transferred (with TP) — or owned — correctly.

Plan for India-specific banking quirks. Inward remittance documentation (FIRC, KYC) takes time. Open the bank account early.

Don't underestimate FEMA. It is the single most under-respected statute by foreign founders entering India.

Banking, Repatriation, and Transfer Pricing

Three areas that separate good India entries from painful ones:

Banking: Open a current account with a scheduled bank early. Submit complete KYC + MOA + AOA + board resolutions. Indian banks are conservative on inward remittances; allow 2–3 weeks for the first remittance.

Repatriation: Dividends, royalties, management fees, and capital reductions are all repatriable — but only when documented correctly under FEMA. Use a 15CA / 15CB workflow for every overseas remittance.

Transfer Pricing: Every related-party transaction must satisfy the arm's-length principle, supported by a benchmarking study. Form 3CEB filed annually. TP penalties run up to 2% of the international transaction value plus interest. This is not the place to cut corners.

Planning your India entry?

Jordensky has helped 100+ foreign companies set up, scale, and stay compliant in India — across SaaS, manufacturing, fintech, and services. We handle entity formation, FEMA, FDI reporting, tax structuring, transfer pricing, and outsourced CFO under one roof.

Book a Free India Entry Consultation → a 30-minute call with a Mumbai-based CFO and tax advisor. No commitment. Strategic insights, not a sales pitch.

Frequently Asked Questions

1. Can a foreign company own 100% of an Indian company?

Yes — in most sectors via the automatic route. Some sectors (defence, insurance, multi-brand retail, etc.) have caps or require government approval. Always check the current DPIIT FDI policy.

2. What is the best entity for a foreign company in India?

For 80%+ of cases, a wholly-owned subsidiary (private limited company). It earns revenue, hires staff, raises capital, and signals long-term commitment. LLPs work for sectors with 100% automatic FDI; liaison offices are only for non-revenue presence.

3. How long does it take to register a company in India?

A wholly owned subsidiary typically takes 3–6 weeks end-to-end if FDI is on the automatic route. Approval-route entries take 8–12 weeks

4. What taxes do foreign companies pay in India?

Indian subsidiaries pay corporate tax at ~25.17% (under Section 115BAA). Foreign companies operating directly via a branch pay ~38%–42%. GST, TDS, PF/ESI, and transfer pricing apply. Dividends are taxed in the shareholder's hands (subject to DTAA).

5. Do I need a resident director to incorporate in India?

Yes. At least one director must be a resident of India — meaning they have stayed in India for 182+ days in the previous financial year.

6. What is FC-GPR, and why is it important?

FC-GPR (Foreign Currency – Gross Provisional Return) is the FEMA filing that reports share allotments to non-residents. It must be filed within 30 days of allotment. Missing it triggers compounding penalties.

7. Can a foreign company open a liaison office in India?

Yes, with RBI approval. A liaison office cannot earn revenue or invoice clients — it's limited to representation, market research, and communication. Maximum tenure is 3 years (renewable).

8. What is the minimum capital required to start a company in India?

There is no minimum paid-up capital requirement for a private limited company in India (after the 2015 amendment). Many WOSes start with ₹1 lakh authorised capital and infuse working capital later.

9. How is transfer pricing applied to foreign-owned subsidiaries?

Every related-party international transaction must be at arm's length, supported by a benchmarking study and certified annually via Form 3CEB. Penalties for non-compliance can reach 2% of transaction value.

10. Can profits be repatriated from India?

Yes—dividends, royalties, fees for technical services, and capital reductions are all repatriable under FEMA, with proper 15CA/15CB documentation and applicable taxes.

Final Takeaway — India Rewards Structure, Not Speed

India is the most procedural, paper-trail-heavy major market a foreign company will enter — and that is precisely its strength. Companies that respect the process get protected by it. Companies that try to move fast and fix structure later spend the next two years untangling FEMA, transfer pricing, and tax issues that should never have happened.

If you're entering India in 2026, invest the first 30 days in structure: the right entity, the right FDI route, the right tax posture, and the right transfer pricing playbook. Everything you do for the next decade in India compounds off that foundation.

Written by

CA Akash Bagrecha

Co-founder, Jordensky · Chartered Accountant

CFO advisory for 200+ startups and MSMEs. Helped raise ₹400Cr+ across 30+ fundraises. Passionate about building scalable financial operations for India's growing businesses.